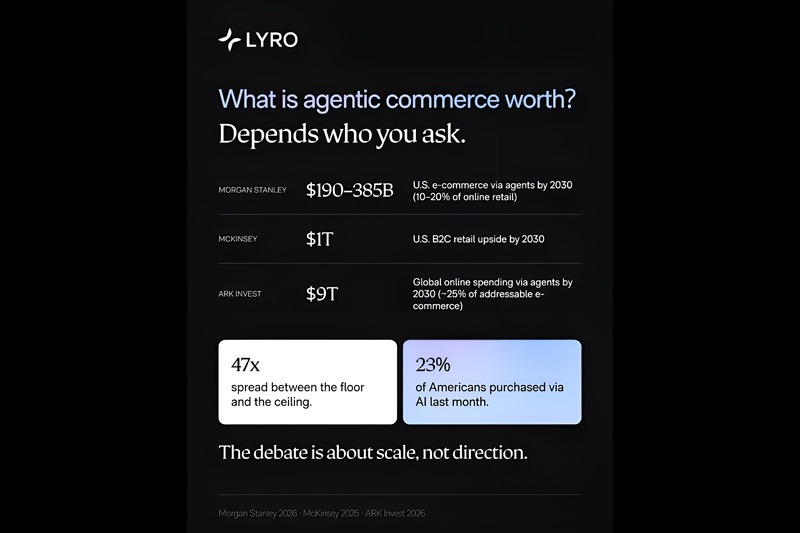

ARK Invest says $9 trillion. Morgan Stanley says $190–385 billion. McKinsey says $1 trillion by 2030. The range isn’t an accident: it reveals exactly where the uncertainty lies, and where the real investment opportunity may be hiding.

Few emerging technology markets have generated a wider spread of analyst projections than agentic commerce: the category covering AI agents that discover, evaluate, and purchase products autonomously on behalf of consumers. Depending on which research house you read, the addressable market by 2030 is either transformative or merely significant. Understanding why the estimates diverge so dramatically is more useful to investors than picking a number to anchor to.

What “Agentic Commerce” Actually Means

Before the projections can be evaluated, the definition matters. Agentic commerce refers to the full stack of AI-mediated shopping: a consumer delegates a purchase task to an AI assistant, which then researches options, compares prices, authenticates with merchants, executes payment, and handles post-purchase service — all without requiring the user to visit a website or app. The infrastructure enabling this includes a new layer of open protocols: OpenAI’s Agentic Commerce Protocol (ACP), Google’s Universal Commerce Protocol (UCP), Visa’s Trusted Agent Protocol (TAP), and Google’s Agent Payments Protocol (AP2), among others. These are not speculative; most launched between late 2024 and early 2026, with backing from Stripe, Mastercard, PayPal, Shopify, and Walmart, among dozens of others.

The technology exists. The consumer readiness is building. The investment question is how fast, and through which channels.

Breaking Down the Projections

ARK Invest: ~$9 Trillion by 2030

ARK’s projection is the most cited and the most misread. The firm estimates AI agents could facilitate approximately $9 trillion in global online spending by 2030, representing roughly 25% of addressable e-commerce. The crucial qualifier: e-commerce itself accounts for only about 20% of total global retail. Run the math and ARK’s bullish scenario translates to roughly 5% of total retail sales — a meaningful but not economy-reshaping share. ARK’s more specific investment thesis centers on digital wallet providers: if 10% of agentic volume flows through digital wallets at a 5% lead-generation fee, that implies $43 billion in incremental wallet revenue, a roughly 50% increase on today’s global wallet revenue base. That is the actual investable claim, and it is considerably more precise than the headline trillion-dollar figure.

McKinsey: $750 Billion in AI-Influenced U.S. Revenue by 2028; $1 Trillion in Agentic Commerce by 2030

McKinsey’s projections address two distinct phenomena that are often conflated. The $750 billion figure refers to U.S. revenue flowing through AI-powered search, meaning purchases where AI tools influenced the discovery phase, not necessarily where an agent completed the transaction. The $1 trillion figure, which applies to U.S. B2C retail by 2030, is the narrower agentic commerce estimate — purchases where AI agents play a more active transactional role. The distinction matters for investors: the first number is already partially happening and affects every e-commerce company through visibility and traffic dynamics; the second is further out and more contingent on infrastructure adoption.

McKinsey also provides the most pointed risk framing: brands that fail to prepare for AI-search distribution risk losing 20–50% of their traditional search traffic. That is not an upside projection. It is a redistribution warning.

Morgan Stanley: $190–385 Billion in U.S. E-Commerce by 2030

Morgan Stanley’s range is the most conservative and arguably the most rigorously bottoms-up. Their estimate represents 10–20% of projected U.S. online retail market share, grounded in observed adoption rates rather than theoretical ceilings. The wide band within their own projection reflects genuine uncertainty about pace, not disagreement about direction. At the low end, agentic commerce is a meaningful niche; at the high end, it is a structural shift in how a fifth of U.S. e-commerce is transacted.

What Explains the Spread?

The divergence across these projections is not noise. It reflects three genuine disagreements about how agentic commerce will develop.

Definition of “agentic.” ARK counts any AI-facilitated transaction; Morgan Stanley applies a stricter standard requiring meaningful autonomous action by the agent. The same consumer behavior scores differently depending on the methodology.

Adoption curve assumptions. Consumer readiness surveys show rapid movement: a longitudinal study by Omnisend found that reluctance to allow AI to handle transactions dropped from 66% to 32% in just five months between early and mid-2025. But behavioral adoption and survey-stated intent consistently diverge, and most of the large projection figures assume continued linear acceleration.

Infrastructure timing. All of the projections assume that the protocol layer — ACP, UCP, TAP, AP2 — reaches sufficient merchant adoption to make seamless agentic checkout widely available. That is not guaranteed. The current landscape has parallel competing standards from OpenAI and Google, and consolidation may take years.

Where the Actual Investment Signal Is

Regardless of which macro projection proves closest, several sub-themes emerge with higher conviction from the current data.

Payment infrastructure providers are best positioned in the near term. The protocols being built require token-based authentication, spending-limit governance, and settlement rails. Visa (TAP), Mastercard (Agent Pay), and PayPal (ACP adoption, Agent Toolkit) are embedding themselves as required infrastructure for agentic transactions. This is not speculative future revenue: these integrations are live or in active rollout now.

Platform-native AI has a demonstrable conversion advantage. During Black Friday 2025, Amazon’s Rufus-assisted sessions resulted in purchases growing at five times the rate of non-Rufus sessions. That is a controlled, first-party data point with direct revenue implications. Retailers with proprietary AI agents embedded in owned commerce surfaces appear to have a structural conversion advantage over third-party agent ecosystems, where consumer trust is significantly lower — Bain research indicates shoppers trust retailer AI approximately three times more than third-party tools.

The “AI shelf readiness” layer is an underappreciated B2B opportunity. For agentic checkout to work, merchants must provide structured, real-time product feeds with accurate inventory, pricing, and variant data. OpenAI’s own benchmarks show ChatGPT Shopping Research delivers 64% overall accuracy — meaning more than a third of AI product recommendations currently contain errors. Vendors that help merchants achieve feed completeness and structured data compliance are serving a need that exists today, independent of how the macro projections resolve.

Customer service automation is the most immediate agentic deployment. According to Anthropic’s analysis of millions of agent interactions across its public API, software engineering currently accounts for nearly 50% of agentic tool calls, while customer service represents only a small fraction — not because the technology is unready, but because organizational deployment has lagged capability. Companies like Tidio, whose Lyro AI agent handles an average of 67% of incoming customer inquiries autonomously, represent the category of operator that may benefit most from the deployment overhang closing. Research firm Gartner projects 60% of brands will use agentic AI for personalized customer interactions by 2028.

The Bear Case Deserves More Airtime

The optimistic projections dominate media coverage, but the friction points are real. Consumer trust in AI recommendations remains fragile: a global HubSpot and SurveyMonkey study of over 15,000 consumers found only 30% trust AI search results “a lot” or “completely,” and 28% have already stopped purchasing from a brand because of its AI use. Measured AI-referred traffic still represents only 0.2% of total e-commerce sessions, per Contentsquare’s aggregate data. Google delivers over 678 times more human visitors per referral than AI applications, according to TollBit’s analysis of publisher traffic.

The most rigorous academic study on conversion quality, analyzing 973 e-commerce websites with $20 billion in combined revenue, found that ChatGPT referrals converted worse than most traditional channels after controlling for site effects and data sparsity, though the gap was narrowing over the study period.

None of this invalidates the long-term thesis. It does suggest that investors pricing in the ARK ceiling scenario in a two- to three-year horizon are running ahead of where consumer behavior and merchant infrastructure currently are.

The Practical Takeaway

The wide spread in agentic commerce projections is not a failure of analyst rigor — it is an accurate reflection of how much genuinely depends on variables that cannot yet be measured: protocol consolidation, consumer trust dynamics, merchant adoption rates, and regulatory treatment of AI-driven pricing and personalization. The investable opportunities that do not require those variables to resolve favorably are in payment infrastructure, platform-native commerce AI, and the B2B layer supporting merchant data readiness. The macro upside, should the ARK or McKinsey scenarios materialize, layers on top.

Investors who treat this as a single market will overpay for the wrong exposures. Those who decompose it will find the signal in the infrastructure.

This article draws on analysis published in “AI in E-Commerce in 2026: The New Shopping Funnel,” a research report by Lyro.